Taxes & Compliance: The Silent Threat to Kenya’s Healthcare Sector

[Symbolic clash between authority and medical business practice]

Taxes and compliance are not just routine obligations for healthcare businesses in Kenya. They have turned into pitfalls for many healthcare institutions.

1400 private hospitals were closed down by the Ministry of Health for fraudulent billing and malpractice in a 2023 report. Private healthcare facilities account for 54% of the 14883 healthcare institutions nationwide; these closed-down hospitals represent 10% of the institutions. (Kenya Health Facility Census Report, 2023)

This is contrary to the overdue Universal Health Coverage (UHC) goal.

The current tax regime and regulatory framework drain resources, stifling innovation and discouraging investment.

Why Taxes and Compliance are the Biggest Threats:

Taxation

- Heavy taxation and impractical dispute mechanisms.

Healthcare businesses face multiple layers of taxation:

- Corporate tax (30%)

- VAT on medical equipment

- Import duties

- County levies

These costs compound, eroding margins and making essential supplies unaffordable.

Complicating matters further is the taxman (KRA), which has made tax dispute resolution impracticable for many institutions.

- Insurance Paradox

This phrase is coined to refer to a situation where:

- Corporate insurers and the Social Health Authority (SHA) delay reimbursements for 60-90 days

- KRA demands taxes on these uncollected, paper profits.

Example: A Nairobi-based level-4 private hospital recently faced a KES 403 million tax dispute with the Kenya Revenue Authority (KRA).

The Nairobi Hospital entrance. FILE PHOTO | NMG

- Finance Act Amendment Risks

The taxman continually seeks the upper hand in tax dispute cases through annual finance bills.

The Finance Bill 2026 proposes the total deletion of Section 42(14)(e), allowing the Kenya Revenue Authority (KRA) to freeze or seize bank accounts and assets even while a tax dispute appeal is actively ongoing.

The bill tables an amendment to the Tax Procedures Act (TPA)

Under existing law, Section 42(14)(e) serves as a legal shield. It prohibits the KRA Commissioner from issuing enforcement actions to third parties if the taxpayer has formally filed an appeal against a tax assessment.

By deleting this protection, KRA would gain total authority to recover disputed funds immediately after rendering a tax assessment.

This empowers KRA to legally bypass the pending verdict of the Tax Appeals Tribunal or courts. If passed into law, KRA can issue agency notices to clear or freeze funds held by any third-party institution linked to the taxpayer:

- Commercial bank accounts

- Mobile money wallets like M-Pesa

- Saccos and financial cooperatives

- Primary employers

Freezing active operating accounts impedes a company’s ability to pay operational costs, effectively forcing operations to stall while fighting the legal case.

Example:

A mid-tier private healthcare faced temporary agency freezes and account embargoes by the KRA.

The clinic downsized its maternity ward, cut staff, and delayed upgrading its electronic medical records to meet KMPDC licensing standards. (https://willowhealthmedia.org/, September 2nd, 2025)

Compliance Burden:

From SHA accreditation to Pharmacy & Poisons Board licensing, the compliance burden is heavy.

Small and medium healthcare enterprises (SMEs) often lack the resources to keep up, exposing their operations to legal issues.

To register a private clinic (Kenya Essential Package for Health (KEPH) Level 2), the specific requirements span approximately 15 to 25 total pages across the application and inspection processes.

This means that new entrants struggle to break into the market because compliance costs are front-loaded before revenue is earned.

The structural Impact:

- Limited access to affordable medical supplies.

- Discourage private investment in hospitals and clinics.

- Push SMEs into informality or closure.

- Undermine the government’s own goal of Universal Health Coverage (UHC).

However, these challenges are not limited to the healthcare sector.

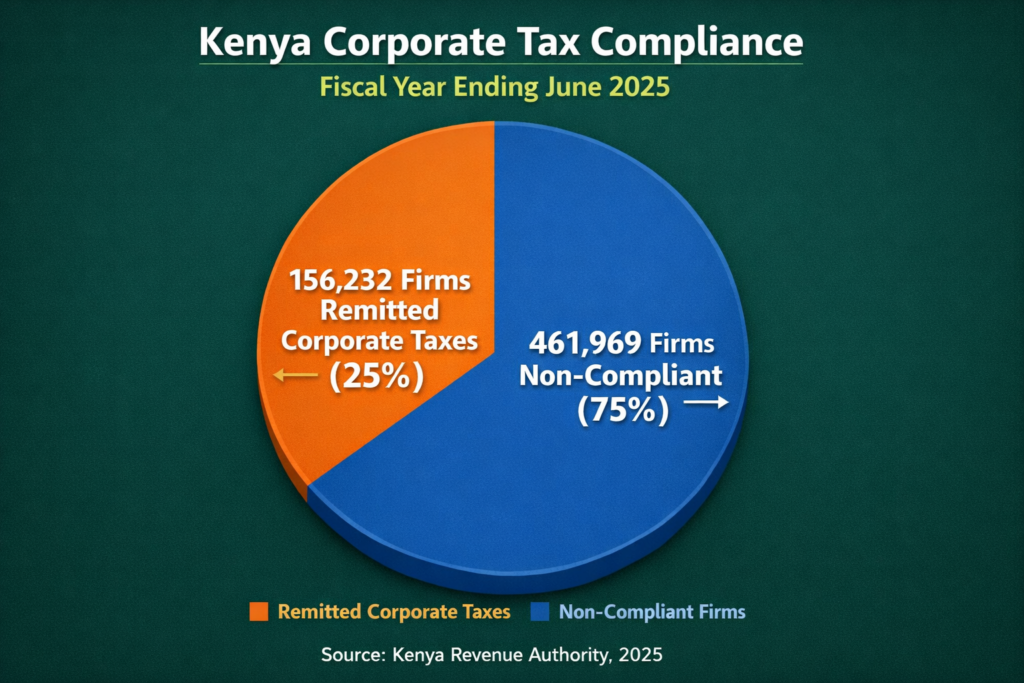

Only 156,232 out of 618,201 registered firms (25%) remitted corporate taxes in the fiscal year ending June 2025, leaving nearly 75% classified as non-compliant (Kenya Revenue Authority, 2025).

Piechart | Data source KRA

Tax Optimization for Healthcare Facilities

The main hurdle for most businesses trying to achieve full compliance under the Finance Act 2025.

The Act requires that all business expenses be supported by an eTIMS-compliant electronic tax invoice to be recognized as a deductible expense.

Costs lacking these invoices are treated as taxable profit, which has triggered major supply chain bottlenecks.

Consequently, clinics and hospitals must invest in payroll software upgrades to avoid penalties, maximize cash flow efficiency, and maintain regulatory alignment.

When buying medical equipment like anesthesia machines, theatre, laboratory equipment, and diagnostic machines in Nairobi, you can deduct these procurement expenses to minimize your tax burden.

For medical equipment purchases, the following depreciation costs are tax-deductible:

- 50% the cost in the first year of use: This applies to hospital equipment, including devices used in your medical startup in Kenya.

- 25% per year on reducing balance: The remaining value is deducted over time

Example in a table: This means if a firm purchases Kes 10 million worth of medical equipment in this category, they can deduct KES 5 million in the first year and KES 2.5 million annually on the remaining balance.

| Year | Deduction Amount | Remaining Balance | Notes |

| Year 1 | KES 5,000,000 | KES 5,000,000 | Initial 50% deduction is allowed on qualifying capital expenditure. |

| Year 2 | KES 2,500,000 | KES 2,500,000 | 25% annual deduction on the remaining balance. |

| Year 3 | KES 2,500,000 | KES 0 | Final 25% deduction completes full capital recovery. |

TAX SAVINGS IMPACT

Based on a 30% corporate tax rate for a firm purchasing KES 10 million worth of medical equipment:

| Deduction Year | Deduction Amount | Tax Rate | Tax Savings | Remaining Balance |

| Year 1 | KES 5,000,000 | 30% | KES 1,500,000 | KES 5,000,000 |

| Year 2 | KES 2,500,000 | 30% | KES 750,000 | KES 2,500,000 |

| Year 3 | KES 2,500,000 | 30% | KES 750,000 | KES 0 |

This means the firm saves KES 3 million in taxes through capital deductions over three years.

This accelerates cash flow recovery and improves investment returns on medical equipment purchases.

For furniture and fittings in your facility, such as hospital beds, ward screens, examination couches, etc, the allowance is 10% per year on reducing balance.

To Maximize Tax Benefits for your medical facility,

You should track:

- Major equipment purchases

- Daily income

- Operating expenses (Use eTims compliant businesses)

- Insurance claims submitted and paid

It is inevitable to be vigilant with accounting, making it an everyday routine rather than a one-time annual stress-and-guessing scene.

Invest in tax-eligible assets

- Put money into items that qualify for big tax breaks, like hospital buildings and medical equipment. You can deduct 50% of the cost in the first year.

Plan your spending

- Buy equipment at the start of the tax year so you can claim the 50% deduction right away.

Stay compliant with KRA

- Make sure your healthcare business is registered with the Kenya Revenue Authority and that you file taxes on time. Missing deadlines can lead to fines and reduce your savings.

Get expert help

- Work with a tax consultant and KRA customer service agent to guide you through the Investment Allowance and other tax benefits for medical facilities in Kenya.

- This ensures you don’t miss out on deductions.

Alternative Dispute Resolution (ADR)

- Resolve tax and customs disputes outside of courts and the Tax Appeals Tribunal (TAT).

- This voluntary, confidential, and cost-effective mediation process must be concluded within 90 days of the facilitator’s written notice.

How the ADR Process Works

- Application: Submits a completed ADR application form with all supporting documents to the Tax Dispute Resolution Office, located on the 7th Floor, Block B, Ushuru Pension Towers, Nairobi.

- Facilitation: The KRA Commissioner appoints a facilitator who manages the discussions. The process encourages open dialogue to reach a mutually beneficial agreement.

- Resolution: Once parties agree, an ADR Agreement is signed and witnessed by the facilitator to finalize the dispute

Disputes Appropriate for ADR

Almost all tax and customs disputes are eligible, including:

- Tax assessments and penalties raised by the KRA.

- Disputes over customs valuation and classification.

Use legal channels to address disputes with KRA.

Businesses that leverage legal channels may prove their cases convincingly.

Picture: KRA headquarters at Times Tower, Nairobi. File | Nation Media Group

KRA lost a Sh3.3 billion claim against the former Java House owner (www.businessdailyafrica.com, May 2026)

Practical Steps for New Entrants

Step 1: Register Your Business

- Use the Companies Act or the Business Names Act. This makes you eligible for tax benefits.

Step 2: Keep Detailed Records

- Maintain records of all capital expenditures, including:

– invoices, proof of purchase, and installation dates.

Step 3: File Your Tax Returns

Claim Investment Allowance via the iTax portal- Include details of your capital expenditures to claim the Investment Allowance.

Step 4: Consult a Tax Professional

- Ensure compliance with the Finance Act to optimize tax burden.

Step 5: Monitor Changes in Tax Laws

- Stay updated on amendments to the Finance Act to take advantage of new tax benefits for medical facilities in Kenya.

At Kans Med Supply LTD, we understand the chokehold taxes and compliance placed on healthcare businesses. That’s why we:

- Provide compliance-ready medical supplies

- Offer transparent documentation for eTIMS and tax deductions

- Support SMEs with multi-angle, labeled product listings for clarity

Partner with Kansmedsupply today to safeguard your healthcare business against tax and compliance pitfalls.